The governing market traits "regime" changed in late 1Q26, showing more investor concern.

A market "regime" is defined by the governing set of traits and conditions that investors are subject to. You may have heard several terms previously that are types of regimes: bullish, bearish, risk-on, risk-off, etc. To better illustrate this concept, picture yourself driving on a long-distance trip.

How do you feel: alert or tired? Do you want to keep going according to your plans or stop for a while? This is like the investor, whose sentiment may differ depending on any number of factors.

How are the roads? Is the terrain straight and smooth, or are there curves, hills, &/orother obstacles ahead that may make you want to slow down? Do you want to look at an alternate route? This is like evaluating the equity markets: past conditions may not indicate how the conditions are ahead. Do you change your strategy or maintain the course?

How is the weather? Sunny with a clear forecast, or cloudy with a chance of gusting wind and thunderstorms later? This is like evaluating the economy. These are conditions that you have to deal with that you have absolutely no control over.

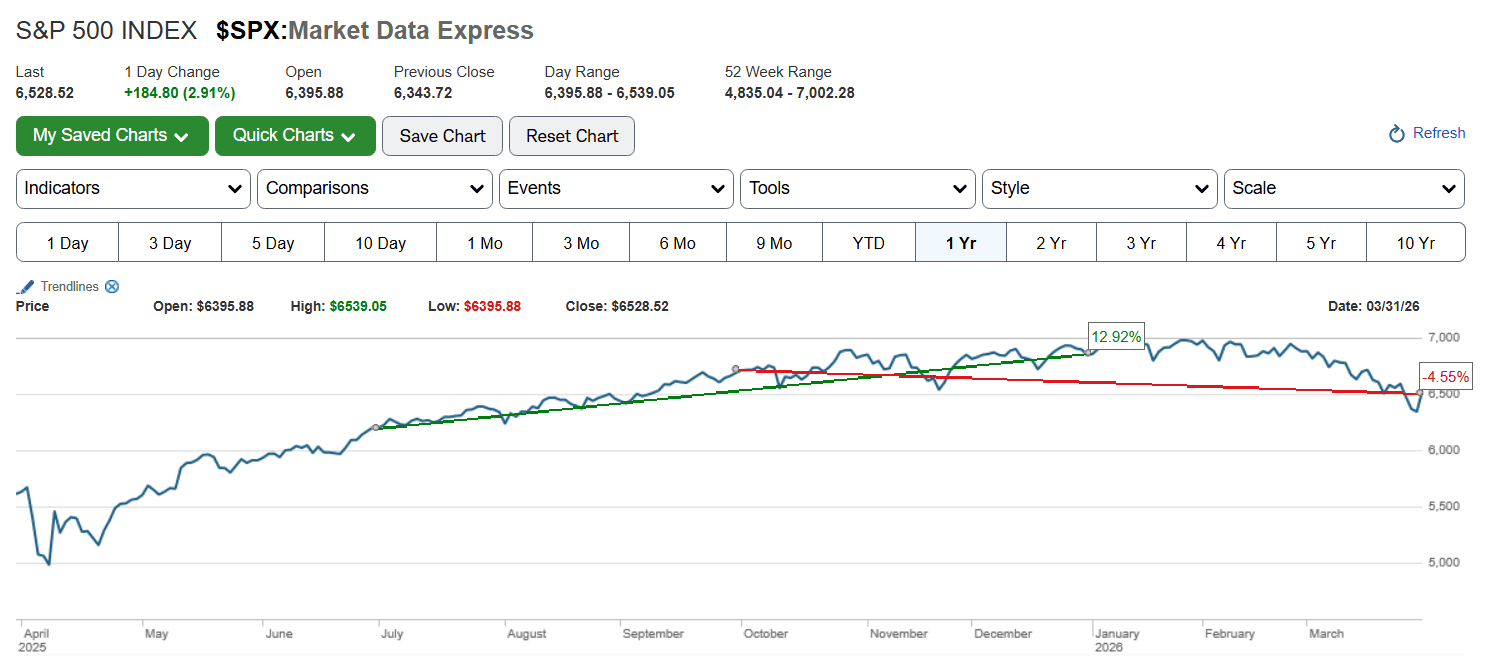

The chart's green line shows the growth of the S&P 500 for 3Q25 & 4Q25. However, the red line shows how the market performed during a rolling two-quarter period, from the start of 4Q25 to the end of 1Q26. The market regime changed from a bullish to a bearish state, with both flat market & economic trends as well.

Looking back over the last six months (October 2025 – March 2026), we observe a distinct "arc" in market performance.

4Q25 =Steady appreciation, fueled by AI capital expenditures and strong year-end earnings.

Early 1Q26 = All-Time Highs. The index peaked above 7,000; optimism regarding a "soft landing" was at its zenith.

Late 1Q26 = Persistent Weakness. Geopolitical escalation and oil price shocks (breaching $100/bbl) led to a ~2.8% decline in March alone. The trend has transitioned from momentum-driven growth to volatility-driven contraction, with the 10-year Treasury yield climbing back toward 4.48%, reflecting a total reversal of the sub-4% expectations held only months ago.

Soft Data: The Pessimism Gap

In contrast to the steady GDP numbers, "soft" sentiment data is flashing red.

- Consumer Sentiment: The University of Michigan index fell to 53.3 in March, its lowest since late 2025. Consumers are feeling the "inflationary impulse" of rising energy costs, with year-ahead inflation expectations jumping from 3.4% to 3.8% in a single month.

- Business Outlook: While AI-focused firms remain optimistic, broader small-business sentiment is weighed down by the elimination of expected Fed rate cuts, with markets now pricing in a potential "hawkish hold" or even a slight hike to combat energy-driven inflation.